From California to Maine, fleets are Googling “cheap commercial auto insurance.” The search volume tells us something important: the gap between what insurers charge and what fleet managers are willing to pay is widening.

Still, insurers argue that premiums need to rise because claims are increasingly expensive. Meanwhile, fleets struggle to understand why they keep paying more year after year.

But here’s the truth: many fleets absolutely DESERVE better rates, especially when they’re pouring resources into safety, actively improving their risk profile, and have the data to prove it:

- 73% of fleets reported improved driver safety with dashcams

- 72% saw fewer crashes and claims when combining telematics with training

- 74% use telematics data for driver coaching

- 48% reduced crash costs reported

- 30% drop in claim frequency & severity (Amerisure)

When such fleets type “cheap insurance” into Google, they’re not looking to cut corners. They’re looking for a fair price – an insurance program that conforms to their safety profile. They've made investments in technology and training, and they rightfully expect ROI.

Reality check: Why safety investments don’t easily translate into more affordable insurance

So, if these fleets have earned a better rate, are they getting it? We wish it were different, but the answer is:

- Not always.

- Why?

- Because insurers struggle to validate the impact of these investments.

A fleet’s unique safety story becomes a single voice in a sea of submissions, as underwriters lack the tools to easily access and digest the data. Without it, underwriters price based on averages, with a markup for uncertainty.

This is where the law of large numbers works against safe fleets. In an overall unprofitable insurance market, high-performing fleets end up subsidizing the riskiest ones. By shopping around, fleet operators try to avoid the price hike. What they should do is try to escape the high-risk pool they are drowning in.

And here’s the way out:

PROVE your superior risk profile with credible data, instead of TELLING a story.

The shift in perspective: From a quick fix to a long-term advantage

In most cases, asking “How do I get cheaper insurance NOW?”, you are already late. Better ask, “How do I build a case for more affordable insurance at my NEXT renewal?”

Switching carriers with the same old submissions is like handing different teachers the same test paper – you’ll get the same grade, no matter who marks it.

The real path to more affordable insurance is to make your safety investments visible, verifiable, and usable by insurers. It means proving your low-risk profile with clean, contextualized data and sharing it with the people who determine the price.

This isn't about a shortcut for today; it's about a strategy for tomorrow.

How Draivn helps fleets do this

Draivn provides tools to leverage fleets’ operational and safety data to qualify for the best-suited insurance program. Here are just a few insurance-related problems Draivn solves to improve your bottom line.

Problem: Messy submissions and inconsistent data lead to higher premiums

Solution: Draivn harmonizes, normalizes, and enriches fleet data with context, creating a single source of truth that your broker can use to advocate on your behalf and negotiate prices with confidence – proving your low-risk profile with facts.

Problem: Submissions get lost in the insurer’s inbox, and it costs you money

Solution: Draivn’s EZ Quote intelligently matches your risk profile with insurers’ appetites. Your perfectly structured submissions will reach the insurers that are most likely to want your business in the format they prefer. This dramatically improves your first-look chances, speeds up underwriting, and increases your chances of receiving the most competitive quote on the market.

Problem: Fleets lack a clear view of their own risk, holding back safety improvements

Solution: Draivn’s dynamic fleet risk profile dashboard provides a 360° view of risk – driver behavior, exposure, operations, and comparative benchmarks. It directly connects how your fleet operates to how it’s perceived by insurers, providing actionable insights to improve that perception and get better insurance rates at your next renewal.

Problem: Manual data collection drains resources

Solution: Draivn automates data collection and allows secure sharing of vehicle, driver, and exposure information with your broker and insurer. Submissions are pre-filled, saving dozens of man-hours and reducing costs associated with insurance administration.

Safety + data visibility = savings for all

The industry needs to shift from an "everyone must pay more" mindset to one that rewards safety. The high cost of insurance isn't driven by low prices; it's driven by the rising cost of accidents and legal involvement. That cost is priced into every policy.

Fleets that can prove they’re safer deserve to pay less. And when they make their safety data visible, the results are clear:

- 10%-25%+ lower premiums, or evenup to -50% in deductibles in real cases(McKinsey, DF Carrier, XYZ Logistics)

- Crash liability reduced by 60% as reported by a Mix Telematics client.

- 44% reduced insurance costs

Conclusion

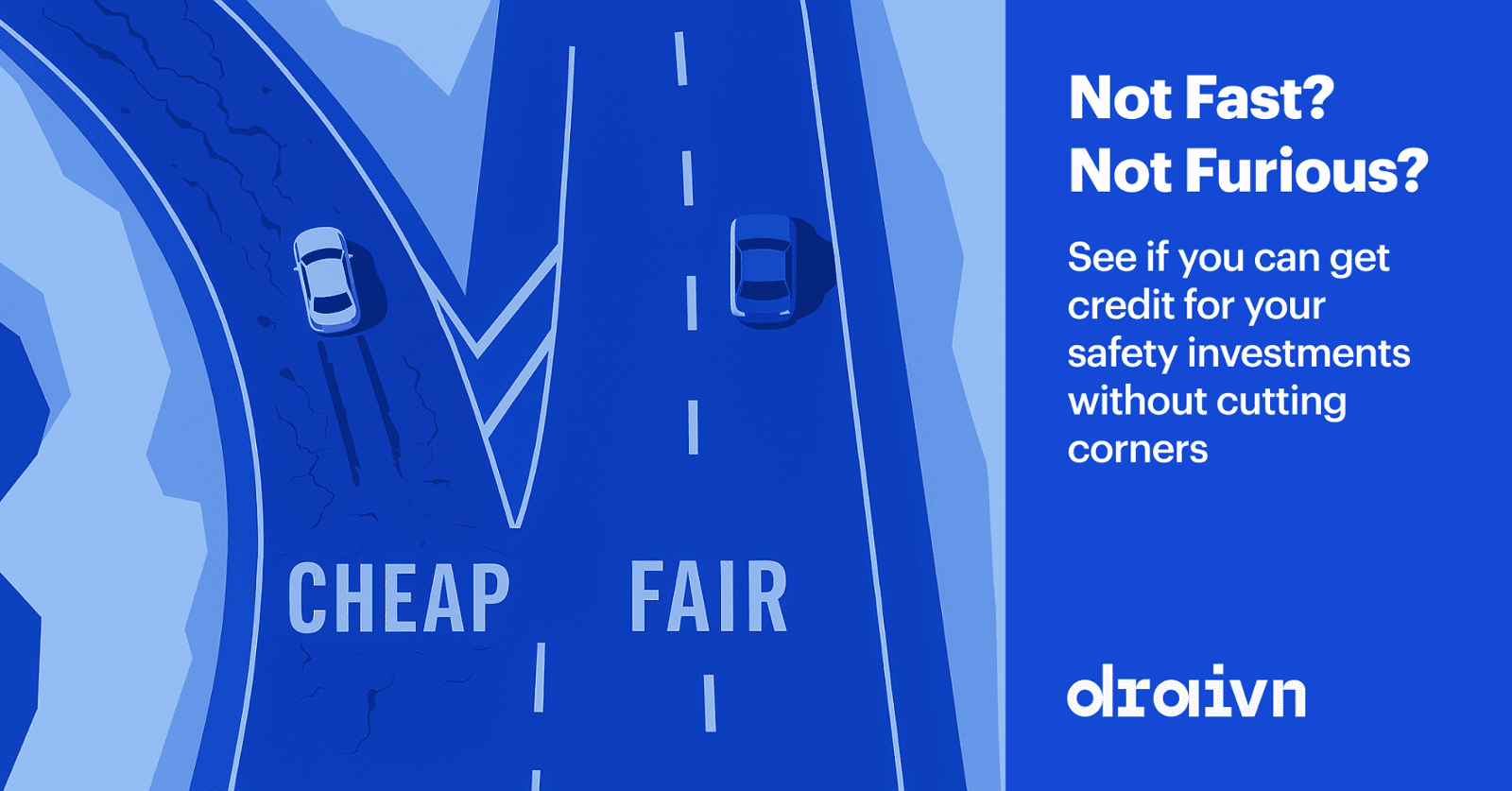

So, is it “cheap” commercial fleet insurance that you need? Or fair insurance that reflects your true risk profile?

Draivn helps fleets earn rewards for safety investments and translate data into savings. And there are no hidden pitfalls:

- You own your data.

- Sharing is secure and transparent.

- It’s free to start.

Ever wondered whether you’re getting full credit for your safety investment? Ask your broker how Draivn can help.